The Westpac Massey University Fin Ed Centre has released its 2019 New Zealand Retirement Expenditure Guidelines showing a continuing shortfall between NZ Superannuation and actual household expenditure. A two person household in provincial New Zealand had the smallest income gap while households in Metropolitan areas wanting a ‘choices’ lifestyle had the largest shortfall.

The estimated retirement capital required to fill the gap is estimated to be a hefty $764,000 for a single person wanting a ‘metro choices’ lifestyle and $787,000 for two persons.

How to accrue capital to fill the gap?

The report recommends people start saving early but also that it is never too late to start. Any savings are better than none.

For many people their KiwiSaver savings will provide a significant lump sum for their retirement which is why optimising your KiwiSaver account is so important. This means taking on age appropriate risk, assessing long term performance and fees and increasing contribution rates if you can. The expanded range of contribution rates are now 3%, 4%, 6%, 8% and 10% although it is worth considering alternative savings vehicles at higher savings levels.

Households living mortgage free in their own home generally have a smaller retirement income gap than those who rent or still have a mortgage. Early payment of mortgage debt can be an important part of retirement planning especially if it allows several more years to save the mortgage payments. In future years ‘downsizing, moving to a cheaper housing area or a reverse equity loan can also boost retirement capital.

Other ways to mitigate the retirement income gap include delaying retirement or working part time in retirement.

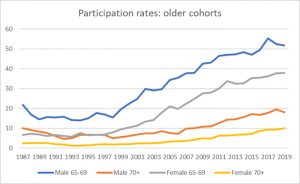

New Zealand labour participation statistics show many Kiwi’s already make this choice with the over 65s having increasing labour participation rates despite being eligible for NZ Superannuation.

Source Michael Reddell blog 11 11 19, based on Household Labour Force Data.

New Zealand has the fourth highest labour participation for those aged 65 -69 in the world, behind Iceland, Japan and Korea. One explanation is that NZ Super is a universal benefit paid at age 65 to New Zealand residents meeting the residency criteria1; there is no disincentive to stop working on receipt of Super.

There is considerable research that remaining engaged in the workforce and/or community is positive for human longevity however the significant fall in interest rates is likely to be a more practical reason for retirees to continue working.

The report states that within ten years the entre Baby Boomer cohort will be over 65. This has real implications for the sustainability of NZ Super.

For those wanting to get a jump on the retirement income gap, talk to one of Saturn’s financial advisers for sensible, impartial advice.

1. Currently 10 years in total since age 20, with 5 years since age 50.